ASX 300 Updates

Please click the dated tabs below to review the updates.

To receive our email updates on ASX reporting season as they’re sent out, subscribe using the form in the right column (desktop) or below (mobile).

2025

2025 AGM Season Highlights Rising Investor Expectations on Pay Alignment

Remuneration report voting outcomes from the 2025 AGM season confirm that investors are applying tougher tests to executive pay outcomes. Shareholders are no longer assessing remuneration in isolation — they are judging whether pay outcomes genuinely reflect performance, shareholder experience and the sustainability of results delivered.

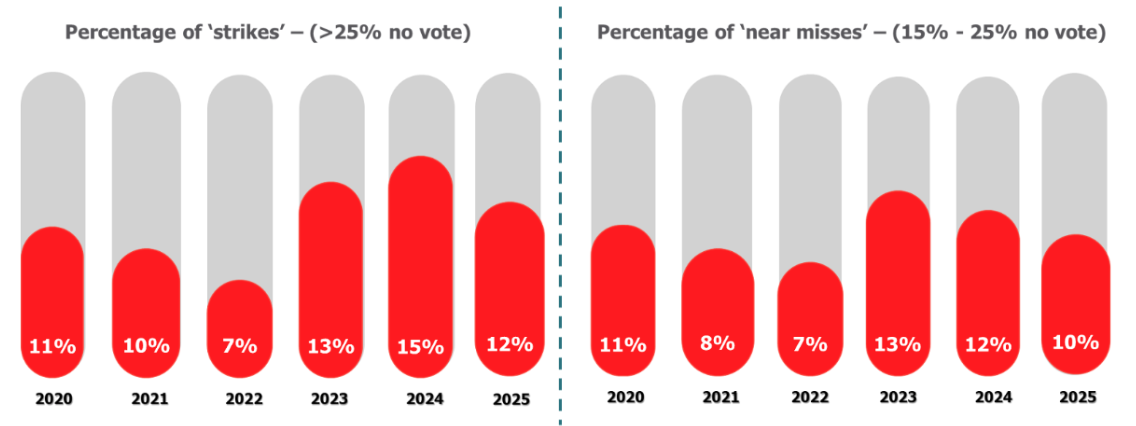

While overall strike levels remain above long-term averages (see Figure 1 below), the defining feature of the 2025 season is not the volume of dissent, but its intensity and concentration. Sector exposure, earnings volatility and board responses to prior shareholder feedback are increasingly determining voting outcomes — with WA-based companies standing out (for the wrong reasons) this year.

Figure 1: Remuneration Report Voting for ASX 300 Companies

Why shareholders continue to vote against remuneration reports

While overall levels of shareholder dissent in 2025 were broadly consistent with recent years, the reasons for opposition remain clear and recurring.

Across companies receiving strikes, shareholders most commonly objected to:

- Pay outcomes remaining high despite weak or volatile share price performance, including companies such as IDP Education and CSL where incentive outcomes continued to attract strong opposition based on lack of shareholder returns.

- Incentive outcomes being materially higher due to external or cyclical factors, particularly commodity price movements, rather than management actions — a key concern for a number of Materials and Energy companies. This includes Champion Iron and James Hardie.

- Limited or incremental changes following earlier shareholder feedback, most notably in companies such as Dicker Data and NRW Holdings, both of which went on to receive further consecutive strikes.

- Insufficient explanation of how mixed or poor performance was taken into account, particularly where discretion was applied without a clear framework or reference to shareholder experience.

These voting outcomes suggest investors are less concerned with technical remuneration mechanics and more focused on whether boards are exercising judgement in a way that feels commercially and reputationally credible.

More decisive “No” votes point to deeper dissatisfaction

Beyond the number of strikes, a notable feature of the 2025 AGM season was the increase in very high levels of opposition, with more companies receiving ‘No’ votes in excess of 70%.

These outcomes were often a signal of:

- Strong and coordinated investor conviction

- Concerns that extend beyond single-year outcomes

- Frustration with how boards have responded to previous feedback

Where opposition reaches these levels, shareholders are effectively signalling a loss of confidence in the board’s remuneration oversight, increasing both reputational risk and the likelihood of further escalation in future years.

In the context of a significant “No” votes, a Strike is no longer a warning – it’s a verdict.

WA companies face heightened scrutiny

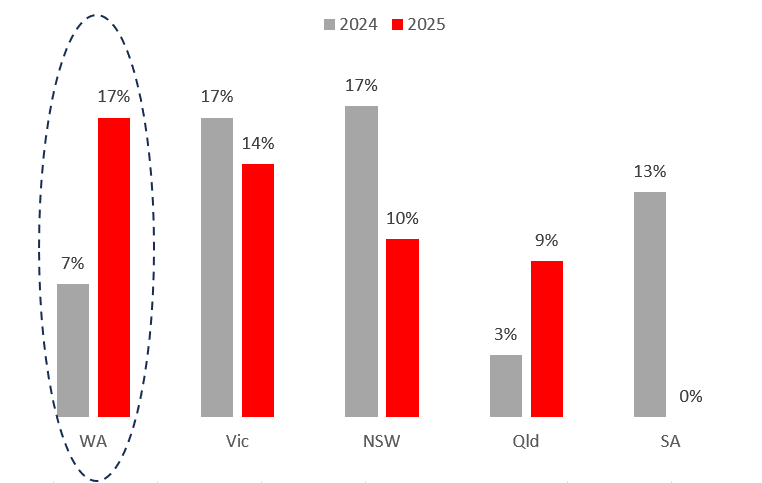

Companies headquartered in Western Australia recorded a material increase in remuneration report strikes in 2025, moving from the middle of the pack in 2024 to the highest strike rate nationally (refer Figure 2 below).

Figure 2: Proportion of ASX300 Companies Receiving A ‘Strike’

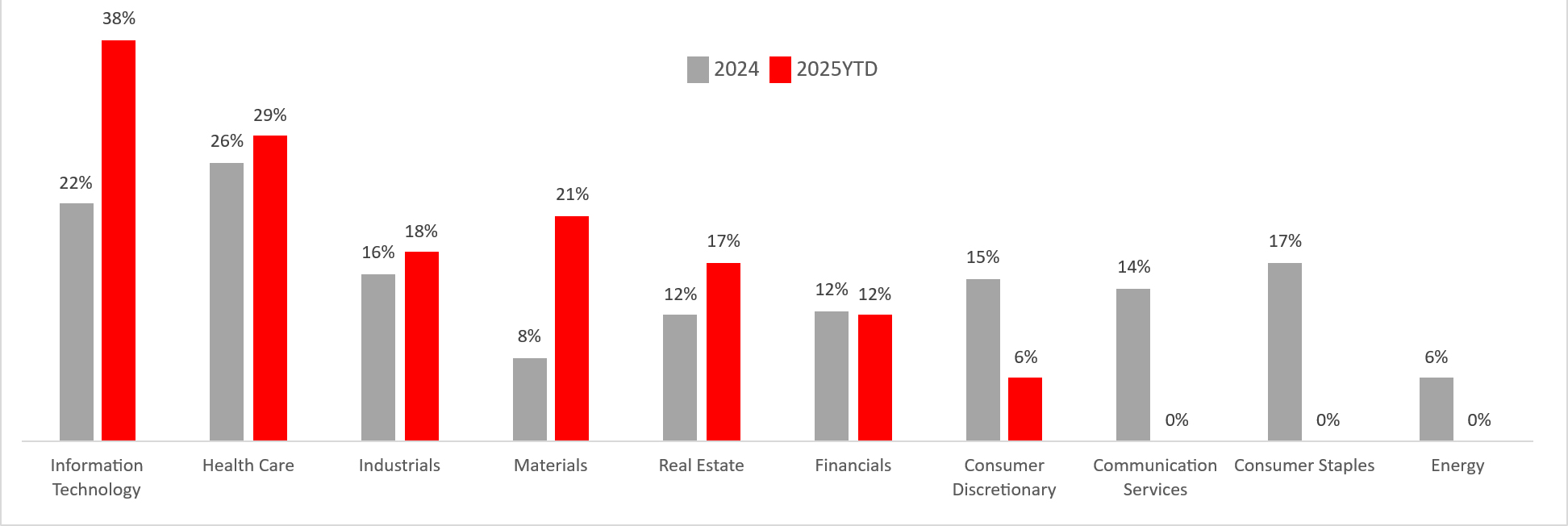

This outcome largely reflects WA’s industry profile, particularly its concentration of Materials and Energy companies, both of which experienced higher strike incidence this year (see Figure 3 below). However, the WA results also point to a broader issue: strong earnings and cash flow (e.g., indicative of many resources companies this year) are no longer sufficient to secure shareholder support for remuneration outcomes. Shareholders are increasingly distinguishing between results driven by market cycles and value created by management decisions.

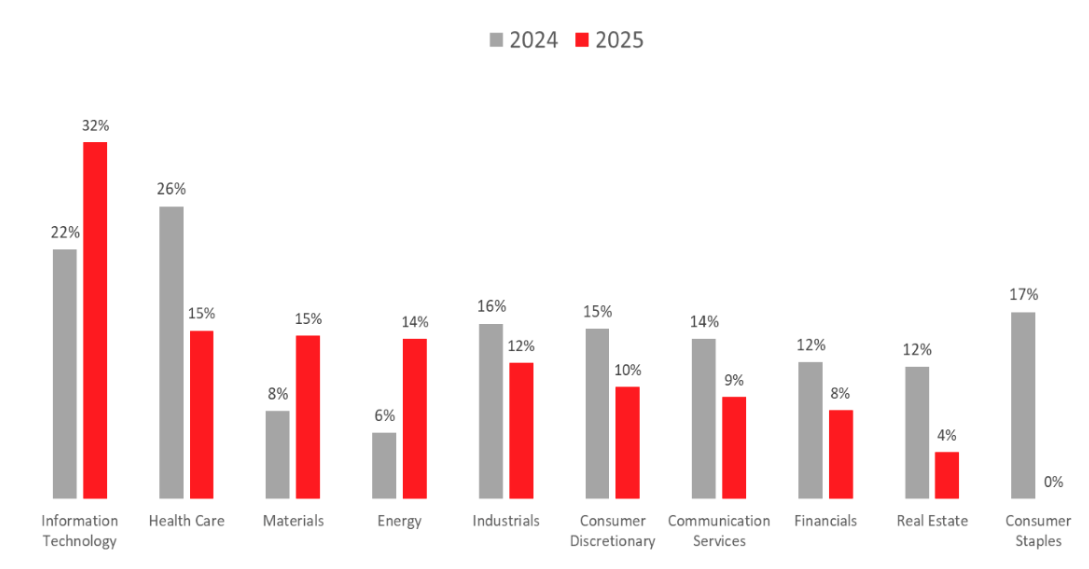

Figure 3: Percentage of Companies Receiving A ‘Strike’ By Sector

Information Technology under increasing pressure

Information Technology recorded the highest proportion of strikes of any sector in 2025, increasing significantly from 2024.

Common shareholder concerns included:

- Incentive outcomes not aligning with shareholder returns (e.g., BrainChip)

- Ongoing reliance on growth targets despite pressure on margins (e.g., Appen)

- Pay structures that had not evolved as businesses matured (e.g., Dicker Data)

This indicates that investors are becoming less patient with pay frameworks that were designed for earlier growth phases but no longer reflect current performance realities.

Repeat strikes point to unresolved issues

A number of companies received a consecutive strike in 2025, most notably:

- Lovisa (4 consecutive strikes)

- Dicker Data (5 consecutive strikes)

- NRW Holdings (8 consecutive strikes)

In each case, shareholders had raised similar concerns to last year, suggesting:

- Changes made after the first strike were either too modest, or

- Were not clearly explained in the remuneration report

Shareholders appear to be looking for clear evidence that boards have addressed the underlying issues, rather than making incremental or technical adjustments.

Looking ahead

Looking ahead, the 2025 AGM season suggests investor tolerance for poorly explained or weakly aligned pay outcomes is continuing to narrow. Boards should expect increased scrutiny where remuneration outcomes appear disconnected from shareholder experience, particularly in volatile or cyclical sectors.

For WA-based companies, the rise in strikes in 2025 indicates investors will be especially focused on whether boards have meaningfully re-calibrated incentive frameworks — not just adjusted outcomes.

Companies that fail to demonstrate clear learning from prior dissent risk entrenching opposition rather than resolving it.

Shareholder Scrutiny Intensifies: Preliminary Insights from the 2025 AGM Season

Australia’s “two strikes” remuneration regime puts significant power in the hands of shareholders. Under the Corporations Act, if 25% or more of eligible shareholders’ votes cast at an Annual General Meeting (AGM) are against the remuneration report, the company receives a strike; if a strike is received in two consecutive years the board must face a spill resolution. This framework makes the annual vote on executive pay more than a formality – it is a barometer of shareholder confidence in how boards align pay with performance.

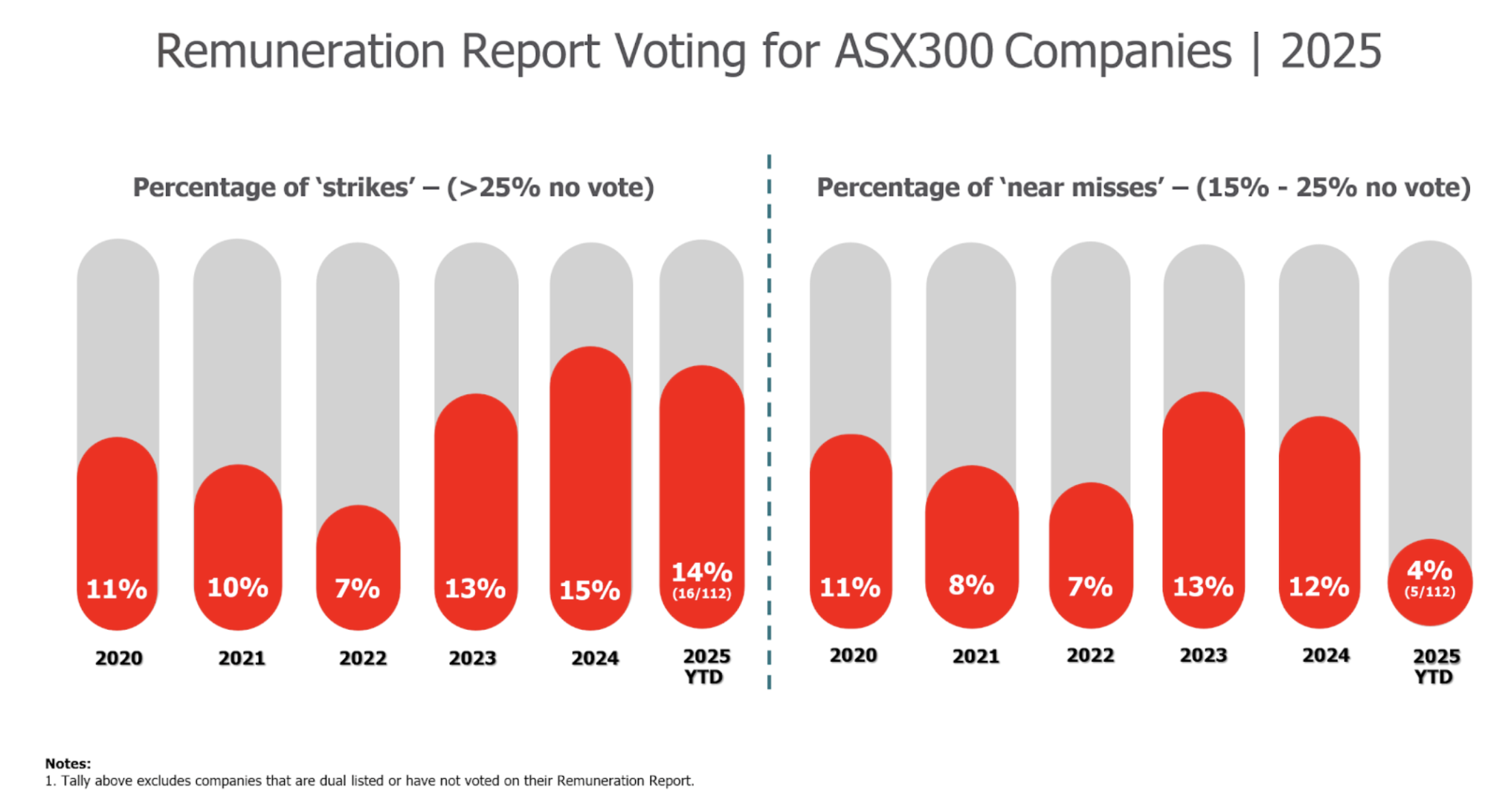

2025 Highlights so far

Up to 20 October 2025, 112 of the ASX 300 companies have held their 2025 AGMs.. Of which 16 remuneration reports (14%) have attracted strikes. Five companies (4%) recorded “near misses”, with 15%–25 % of votes cast against their remuneration reports. These near miss votes do not trigger the two strikes rule but serve as an early warning of brewing shareholder dissatisfaction.

Concentration in a few Sectors

The majority (80%) of companies which have received a strike are in the materials, technology, industrial and financial services sectors.

The following chart compares the share of strikes by sector in 2024 against the 2025 year-to-date figures. The prevalence of strikes in the materials and information technology sectors are up markedly at this stage of the AGM season. Our analysis shows that both sectors are already approaching last year’s full strike counts, despite the season still having another a month to go. . So far, one-third of materials companies and half of information technology companies in the ASX300 have completed their AGMs, recording four of 24 and three of nine strikes respectively – nearly matching 2024’s totals of five (out of 64) and four (out of 18). This reflects increasing scrutiny of pay practices over these sectors.

Percentage of Companies who have received a ‘Strike’ by Sector

Reasons for receiving a ‘Strike’

Some recurring themes behind shareholder opposition. Most companies received their “strike” based on the common themes of perceived pay–performance misalignment, excessive executive pay levels and potentially limited transparency and communication. Examples included the following:

- Orora (48.38% no vote) due to shareholder frustration over executive pay levels and the underperformance of the Saverglass division, acquired in 2023.

- Cleanaway (40.68% no vote) due to investor concerns over safety governance, following three fatalities in FY25 and another in FY26. Despite a 30% reduction in STI payments, a substantial proportion of shareholders voted against the report, citing weak accountability and inadequate board response.

- Macquarie Group (25.40% no vote) received a first strike, driven by regulatory controversies, high executive payouts despite compliance issues, and concerns over risk alignment and transparency in remuneration structures.

- Xero Limited (48.74% no vote). The backlash centred on CEO Sukhinder Singh Cassidy’s USD 15.2 million pay package, benchmarked against U.S. tech peers, which investors and proxy advisers deemed excessive and misaligned with the Australian market.

Companies with Consecutive Strikes

Roughly 40% of the companies that have received a strike so far in 2025 are not first‑timers. These “repeat offenders” have recorded two or more consecutive remuneration strikes, meaning they have faced significant no-votes against their reports in successive AGMs.

- Dicker Data stands out with five straight strikes (76.6% ‘no’ vote). In the last twelve months the Company introduced an LTI scheme to replace uncapped superannuation however the uncapped profit-share cash bonuses continue to be challenged by shareholders given how lucrative it is for executives.

- BrainChip recorded a third consecutive strike (53.9% ‘no’ vote) as shareholders expressed continued frustration over stalled commercial progress and share price performance.

- Champion Iron recorded its third consecutive strike following previous ‘no’ votes of 53.6% (2023) and 32.1% (2024). Opposition likely reflects ongoing shareholder concerns over pay–performance alignment and limited disclosure clarity. Efforts to address feedback in 2025 did not fully rebuild trust.

- Australian Clinical Labs, IDP Education, and Reliance Worldwide each received a second consecutive strike. Despite efforts to address shareholder concerns in their 2025 remuneration reports, the changes did not sufficiently restore investor confidence, reflecting ongoing dissatisfaction with executive pay arrangements and weak pay–performance alignment.

Key Takeaways

The 2025 AGM season underscores that shareholders are increasingly willing to use their say-on-pay rights to demand accountability:

- Align Pay with Performance: Over half of strike companies were flagged for pay–performance misalignment. Boards should ensure incentive structures clearly link rewards to shareholder returns. High fixed pay or short-term bonuses amid weak earnings remain key triggers for large “no” vote campaigns.

- Communicate Clearly: Nearly half of strike companies were repeat offenders, highlighting the need for ongoing, proactive shareholder engagement. Clear explanations of remuneration arrangements, performance metrics, targets, and outcomes can build investor trust and reduce dissent.

- Manage Quantum and Incentives: Remuneration size remains under scrutiny. Boards should benchmark pay to peers and be prepared to justify higher packages with robust business and performance rationale.

- Engage Early: Early engagement with institutional investors – particularly after a “near-miss” (15–25% ‘no’ vote) – can prevent a first strike and demonstrate responsiveness to investor feedback.

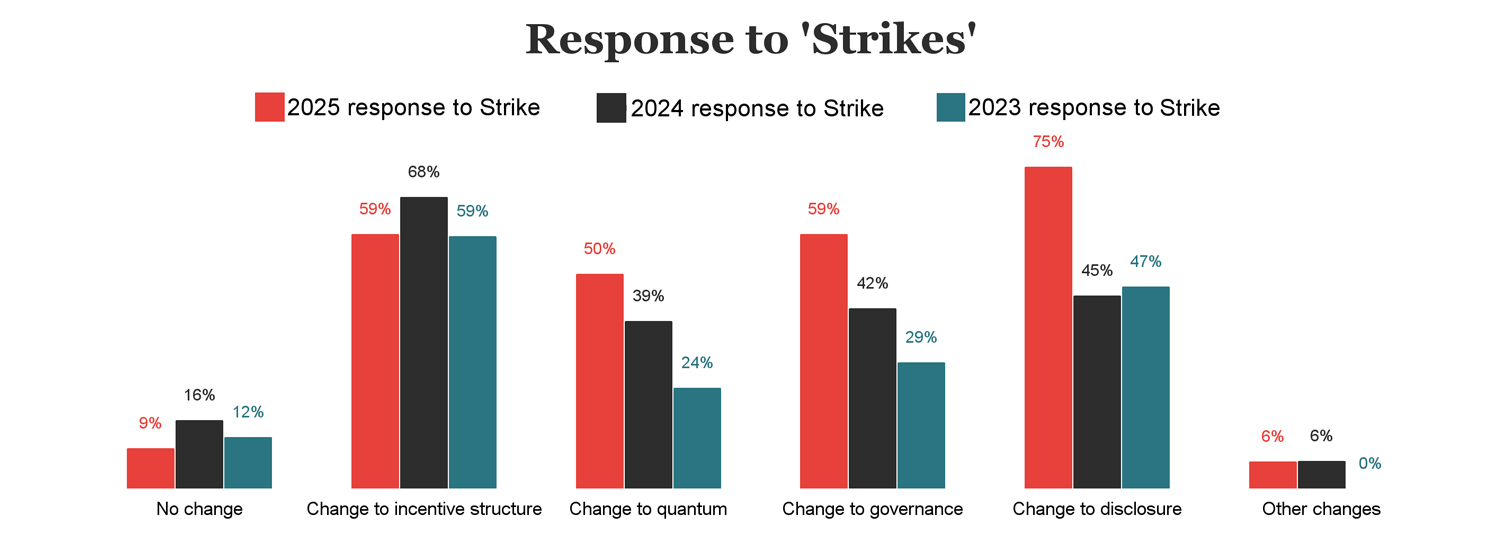

Tracking Strike Responses

With the AGM season about to ramp up, we have conducted our annual research of disclosures in 2025 Annual Reports to understand what actions (if any) have been taken by ASX300 Companies that received a ‘strike’ on their Remuneration Report last year. For those who don’t recall, 2024 had the biggest number ever of ASX 300 companies receiving a ‘strike’ – a total of 15% of the ASX300, breaking the prior record of 13% from 2023. Who knows how much collateral damage there will be in the way of remuneration voting outcomes in 2025.

Of the 32 companies who have responded to a strike from last year so far, 29 (91%) have made changes to address either some or all of the concerns raised by shareholders and / or proxy advisor groups. The remaining three companies have not indicated any changes in response to the shareholder concerns (John Lynas, Lovisa Holdings and Omni Bridgeway). John Lynas and Lovisa Holdings have received consecutive strikes in the last two years and the Board has not made any remuneration changes to address concerns in either year. The 2024 Remuneration Report vote represented the fourth consecutive strike for Lovisa Holdings and the fifth in the last six years!

Note: It is a requirement under the Corporations Act 2001 that the company’s remuneration report include either a description of the actions the Board intends to take in response to a ‘strike’ or an explanation of the reasons for taking no action. See below for details on the 2 Strikes Law.

Strike Responses Tracker

Company responses to ‘strikes’ in 2025 comprised of multiple changes (up to four) to address shareholder concerns (perceived or known). As an example, to strengthen performance and reward alignment, changes were made to equity instrument, performance measures and weighting, adoption of STI gateways, introduction of deferral, and Boards exercised discretion to modify incentive outcomes. In addition to changes to structure and incentive outcomes, companies also enhanced transparency and governance in their remuneration practices by providing additional disclosure of target level setting, introduced clawback provisions and provided more detailed information regarding key performance indicators (KPIs).

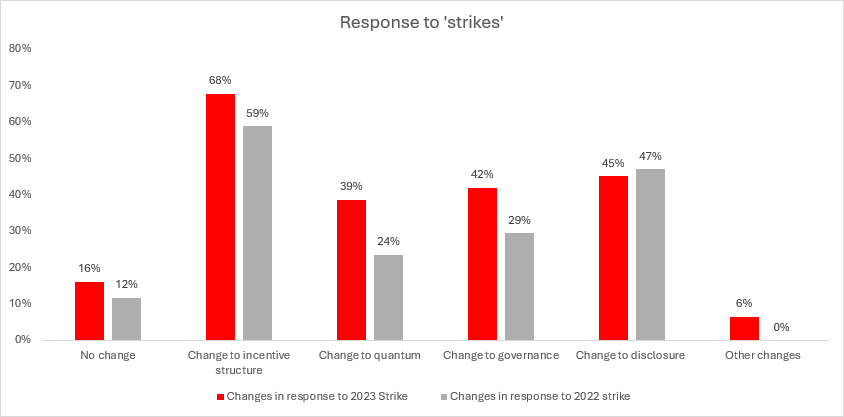

The chart below provides a summary of the response themes adopted by companies to the ‘strike’ on their Remuneration Report over the last three years. Changes to disclosure was by far the most common lever adopted by Boards in response to a strike this year.

Examples of the responses include:

- Change to incentive structure: change in instrument based on shareholder feedback (Dexus Limited), performance metric (Infomedia committing to introduce total shareholder return in FY26), introduction of STI gateway (Australian Clinical Labs Limited, Ingenia), introduction of STI deferral (Dicker Data Limited, Healius Limited).

- Change to quantum: reduced CEO maximum STI (Perpetual Limited, NRW Holdings Limited), reduction in LTI opportunity (Goodman Group), applied downward discretion on variable remuneration outcomes (ASX Limited), changed LTI grant valuation from fair value to face value (Reliance Worldwide Corporation Limited) , halved the STI pool for Executives (ASX Limited).

- Change to disclosure: provision of additional disclosure on STI scorecards (Nine Entertainment Co Holdings Limited), more detail on LTI hurdles (NRW Holdings Limited, Scentre Group), provision of cash-based remuneration table (EVT Limited), greater transparency on metric weightings (Reece Limited) and vesting scales (Mineral Resources Limited).

- Enhanced governance: updated and globally benchmarked remuneration policies (BrainChip Holdings Limited), reinforced discretion approach (CSL Limited), introduction of clawback provisions (Perpetual Limited, Scentre Group, Syrah Resources Limited) and introduced new governance, risk and compliance tools ( IDP Education Limited).

*What is a strike?

If a company’s remuneration report outlining salary and incentives of key management personnel (KMP) receives a ‘no’ vote of 25% or greater from shareholders at the annual general meeting, the company receives a first ‘strike’.

If the following year’s remuneration report also receives a ‘no’ vote of 25% or more, the company receives a second ‘strike’. When a second ‘strike’ occurs, shareholders vote then and there to decide whether company directors must stand for re-election. This is known as a ‘spill’ vote. If the spill vote passes (i.e., 50% or more of eligible votes cast), a spill meeting is held within 90 days and the directors stand for re-election.

See our blog “10 Years On Does The 2 Strikes Law Really Matter?” for more information.

2024

The 2024 AGM Season brought heightened drama as companies faced escalating shareholder dissent hitting a historic record, with 15% of ASX 300 companies receiving strikes on their remuneration reports, up slightly from 13% in 2023. An additional 12% of companies narrowly avoided strikes, reflecting more widespread dissatisfaction.

Key highlights

- Strike Increase: 39 companies (vs. 33 in 2023) faced strikes, representing over 25% of eligible shareholders voting against their remuneration reports. Near misses (15-25% dissent) decreased slightly, compared to 2023 (31 companies).

- Historical Highs: Over a quarter of ASX 300 companies recorded more than 15% dissent on remuneration reports, the highest level since the “Two Strikes Rule” began in 2011.

Standout Themes

CEO Remuneration Under Fire

Investor dissatisfaction centred on the size and structure of CEO pay, particularly variable incentives that were seen as excessive or poorly aligned with performance. Long-term incentives (LTIs) drew criticism for lenient metrics or timelines, while governance lapses in determining pay outcomes added to frustrations.

Notable Companies with High Dissent

- Mineral Resources Limited: 75% ‘no vote’, citing governance issues (first strike).

- Lovisa Holdings Limited: 74% ‘no vote’ (second strike).

- Elders Limited: 68% ‘no vote’ (second strike).

Sector Analysis

- Health Care: Strikes surged to 30% in 2024, up from 8% in 2023, due to concerns over excessive CEO pay and lenient performance targets. Despite talent retention challenges, shareholders viewed these increases as unjustified.

- IT: Strike prevalence dropped significantly to 17% in 2024, compared to 33% in 2023, reflecting improved alignment between pay and performance metrics. Companies in this sector moved away from uncapped cash bonuses and focused on growth with measurable outcomes.

- Communication Services: This sector saw an increase in strikes, reaching 17% in 2024 from 0% in 2023. Shareholders expressed growing concerns over broader executive pay practices and their potential governance implications on decision making.

- Energy and Materials: These sectors maintained the lowest strike rates at 6% and 10%, respectively. Materials improved from 20% in 2023 due to strengthened governance practices and better pay-performance alignment.

Figure 2: ‘Strike’ outcomes by Sector (2024 vs 2023)

Trends in Shareholder Behaviour

Correlation Between Strikes and Market Cap

- Large-Cap Companies: Strikes among large-cap companies (≥ $1bn) slightly decreased in prevalence from 2023 but still dominated the tally, accounting for nearly 75% of strikes in 2024. Among these, 42% experienced dissent rates between 40-75%, reflecting ongoing dissatisfaction with excessive CEO pay and incentive plans.

- Mid-Large Cap Companies: Strikes among mid-large cap companies rose compared to 2023 driven by shareholder concerns over misalignment between pay and company performance.

Figure 3: Distribution of strikes received by market cap (2024 vs 2023)

Perennial Offenders

Since the introduction of the “Two Strike” rule legislation, a growing number of companies have received consecutive strikes. The number of companies receiving second strikes doubled from 5 in 2023 to 10 in 2024, with all Boards avoiding a spill vote. We note that for some companies the strike percentage has been significant in both years (greater than 50%), potentially indicating a systemic issue regarding executive pay outcomes vs shareholder expectations.

Perennial offenders include the following companies who have received more than two consecutive strikes. These include:

- Dicker Data: 2021 – 2024

- Lovisa: 2019, 2021 – 2024

- NRW Holdings: 2018 – 2024

Although the strike counter resets after two consecutive strikes, questions remain about how these companies address persistent shareholder concerns. Proxy advisor influence was noted, underscoring the need for companies to transparently explain their remuneration decisions and deviations from advisory guidelines.

Looking Ahead

Shareholders continue to demand transparency and strong alignment between executive pay and performance. Heading into the 2025 AGM season, companies should:

- Engage proactively and timeously with shareholders to address concerns.

- Disclose detailed rationales for pay decisions, particularly when deviating from proxy advisor recommendations.

- Consider external remuneration advisors, such as TRP, to align pay practices with performance metrics.

The 2024 AGM season’s record dissent reflects shareholders’ growing resolve to hold companies accountable, signalling that robust governance and transparent communication are critical to fostering investor trust.

With over 60% of ASX 300 companies holding their 2024 Annual General Meetings (AGMs) to date, 2024 appears likely to exceed last year’s record number of “strikes” on Remuneration Reports.

Figure 1 below provides a year-on-year comparison of the percentage of ASX300 companies which have received a “strike” (greater than 25% of eligible shareholders voting against) or a “near miss” (between 15% to 25% of eligible shareholders voting against) on their Remuneration Report.

Figure 1: Voting outcomes in 2024 (so far), compared to the previous five years

Tis the Season (of Strikes)

Looking at the strikes received to date, while 22 companies were handed their first strike, 8 faced a second strike. Second strikes require Board members to stand for re-election at a further special meeting, via a ‘spill’ vote. Fortunately, in all instances, companies who received their second strike were able to avoid ‘spill’ votes.

The prevailing focal points for “strikes” on Remuneration Reports in the AGM season so far appear to revolve primarily around generous remuneration packages relative to company performance; soft incentive targets; and opaque report disclosures. These key themes reflect the ongoing challenges associated with aligning remuneration outcomes to company performance and shareholder expectations.

Below are some examples to provide insight into shareholders’ rebukes:

- Perpetual Limited (88% no vote, “First Strike”): Shareholders expressed vehement dissatisfaction around excessive executive pay and retention bonuses (which in some cases, amounted to over 200% of salary). Proxy advisors noted cash retention payments were materially inconsistent with company performance and accepted market practice.

- Goodman Group (35% no vote, “First Strike”): Proxy Advisors indicated that the hurdles to awarding Performance Rights under the company’s Long Term Incentive scheme were “insufficiently challenging”, also citing the approach to excluding share-based payments from the EPS calculation as “unique”.

- Dicker Data Limited (42% no vote, “Fourth Consecutive Strike”): Shareholder concerns included uncapped cash bonuses, short vesting periods for performance-related incentives (assessed and paid either monthly or quarterly) , as well as the CEO’s fixed pay being above the median, relative to peers.

Sector Analysis – Healthcare leading the charge (but early days for Energy & Materials)

Looking at the Remuneration Report voting by sector, leading the ”strikes” to date are Health Care companies (26% have received a ”strike”) followed by Information Technology (17%). Whilst some sectors such as Energy and Materials have received the lowest level of ”strikes”, this may be premature given that more than half of the companies are yet to hold their AGM.

Figure 2 below highlights the percentage of companies per sector which have held their AGM (indicated by the grey bars). The red bars indicate the percentage of ”strikes” received by sector.

Figure 2: Voting outcomes in 2024 (so far), by Sector

TRP will continue to monitor the remuneration report voting and will publish further updates over the coming weeks.

As the AGM season hits full swing, we have conducted research to understand what actions (if any) have been taken by ASX300 Companies that received a ‘strike’ on their Remuneration Report in 2023. This year involves more work than usual, with a whopping 13% of ASX 300 companies receiving strikes last year – the largest since the legislation was introduced in 2012.

Of the 31 companies who have responded to a strike from last year so far, 26 (84%) have made changes to address either some or all of the concerns raised by shareholders and / or proxy advisor groups. The remaining five companies have not indicated any changes in response to the shareholder concerns (Harvey Norman, BrainChip Holdings, John Lynas, Lovisa Holdings and Dicker Data Limited). Interestingly, Lovisa Holdings and Dicker Data have received consecutive strikes in 2022 and 2023 and the Board has not made any remuneration changes to address concerns in either year.

Note: it is a requirement under the Corporations Act 2001 that the company’s remuneration report include either a description of the actions the Board intends to take in response to a ‘strike’ or an explanation of the reasons for taking no action. See below for details on the 2 Strikes Law.

Strike Responses Tracker

Company responses to ‘strikes’ in 2023 comprised of multiple changes (up to five) to address shareholder concerns (perceived or known). As an example, to strengthen performance and reward alignment, changes were made to performance measures and weighting, deferral of awards were introduced, and Boards exercised discretion to modify incentive outcomes. Companies also enhanced transparency in their remuneration practices by providing additional disclosure of group-level targets, and detailed information regarding key performance indicators (KPIs).

The chart below provides a summary of the response themes adopted by companies to the ‘strike’ on their Remuneration Report over the last two years. Changes to variable pay structure was by far the most common lever adopted by Boards in response to a strike in 2023.

Examples of the responses include:

- Change to variable pay structure: change in weighting (AMP Ltd increasing the weighting of financial metrics from 40% to 60%), change in performance metrics (replace absolute total shareholder return to relative shareholder return), increasing the LTI performance period (Atlas Arteria Ltd from 3 years to 4 years), increasing deferral of short term incentive (Magellan Financial Group, Bank of Queensland, Fortescue Metals Group).

- Change to quantum: exercise of Board discretion to modify downward incentive outcomes (Perenti, Sandfire, Qantas), reducing the Non-Executive Director base and committee fees (Tabcorp), reducing the quantum of variable remuneration awards (Platinum Investment Management).

- Enhanced governance: extension of minimum shareholding policy to executives (Nufarm), development of policy for treatment of awards upon termination (Core Lithium), introduction of malus/clawback policy (Lake Resources).

- Changes to disclosure: providing additional disclosure on incentive targets and outcomes (APA Group, Clinuvel Pharmaceuticals, Whitehaven Coal), enhanced disclosure on rationale behind remuneration design (Novonix).

| *What is a strike? The 2 Strikes Law

If a company’s remuneration report outlining salary and incentives of key management personnel (KMP) receives a ‘no’ vote of 25% or greater from shareholders at the annual general meeting, the company receives a first ‘strike’. If the following year’s remuneration report also receives a ‘no’ vote of 25% or more, the company receives a second ‘strike’. When a second ‘strike’ occurs, shareholders vote then and there to decide whether company directors must stand for re-election. This is known as a ‘spill’ vote. If the spill vote passes (i.e., 50% or more of eligible votes cast), a spill meeting is held within 90 days and the directors stand for re-election. See our blog “10 Years On Does The 2 Strikes Law Really Matter?” for more information. |

2023

After a fairly benign AGM season in 2022, ASX300 companies have experienced an unprecedented surge in shareholder ‘no votes’ during 2023, with a record-breaking 13% receiving strikes on their remuneration report and an additional 13% narrowly avoiding the same fate. Certain sectors were particularly impacted feeling the wrath of disgruntled shareholders including Healthcare, Information Technology, and Utilities.

A total of 34 companies received a “strike” (greater than 25% of eligible shareholders voting against). A further 32 companies received a “near miss” (between 15% to 25% of eligible shareholders voting against), meaning more than one in four of ASX300 AGMs resulted in greater than 15% of eligible shareholders voting against the Remuneration Report. These voting statistics indicate the lowest level of support for Remuneration Reports since the “two strikes rule” was introduced in 2011.

Broader Themes This Year:

Amidst the surge in record no votes among ASX300 companies in 2023, investor concerns are broadening their lens of what defines appropriate company performance. Companies faced strikes due to factors including individual project performance, the absence of marketable products, deficiencies in succession planning, and challenging market conditions. This nuanced evaluation by investors reflects scrutiny extending beyond traditional metrics, emphasising the growing requirement for companies to demonstrate excellence in various aspects of corporate strategy and performance. The diversification of reasons behind shareholder concerns further underscores the evolving landscape of investor engagement and governance expectations.

But…The Usual Suspects:

Amid this wave of shareholder activism, traditional themes of concern continued to underpin the voting. Pay and performance misalignment, a lack of perceived stretch in measures and targets, and protest votes against board and company performance have emerged as common themes. Shareholders are increasingly vocal about ensuring that executive remuneration is directly tied to performance metrics that truly reflect the company’s progress and success.

Big ‘No Votes’ Send Clear Message to Big Names:

An unprecedented 12 companies in the ASX300 were on the receiving end of substantial ‘no votes’ from over half of their shareholders. Notable names with significant shareholder dissent included Qantas (83% ‘no vote’), Harvey Norman (82% ‘no vote’) and Elders (63% ‘no vote’). Other ‘strike’ recipients included Fortescue (52% ‘no vote’ citing concerns over quantum of remuneration paid to former key management) and Woolworths (28% ‘no vote’ linked to executives receiving their incentives despite the death of two staff in the last 12 months).

Sectoral Disparities:

Within the ASX300, the various sectors have faced distinct challenges. Healthcare, Information Technology, and Utilities sectors have been particularly susceptible to shareholder dissatisfaction.

Industrials also took a significant hit, with close to a third of the companies receiving a no vote greater than 15%. This was exemplified by Qantas, where shareholders expressed dissatisfaction with outgoing executives’ incentives and the company’s involvement in reputation-damaging controversies. Meanwhile, NRW Holdings, also in the industrials sector, recorded its sixth consecutive strike with concerns over CEO’s pay. In contrast, the Materials sector performed partially better, with 18% of companies receiving a near miss or a strike.

The surge in strikes among ASX300 companies in 2023 signals a seismic shift in corporate governance dynamics. Shareholders are flexing their muscles, demanding greater accountability, transparency, and alignment between performance and executive remuneration.

As the 2023 AGM season is now in full swing, we are tracking shareholder voting on the Remuneration Report for ASX300 companies. To date, a total of 94 ASX300 companies have had shareholders vote on their Remuneration Report. Figure 1 below shows a year on year comparison of the percentage of ASX300 companies which have received a “strike” (greater than 25% of eligible shareholders voting against) or a “near miss” (between 15% to 25% of eligible shareholders voting against) on their Remuneration Report. The results to date indicate a reasonable uptick in the number of “strikes” after the strong support received in Remuneration Report voting in 2022.

Figure 1. Voting outcomes in 2023 to date compared to prior years

The prevailing focal points for “strikes” on Remuneration Reports in the early stages of the AGM season so far revolve primarily around board discretion, generous incentives and poor remuneration report disclosure. These key themes reflect the ongoing challenges associated with aligning performance, remuneration outcomes, and shareholder expectations. Some examples include:

- Nufarm Limited (47% no vote): Shareholders expressed dissatisfaction with the board’s chosen pay incentive strategies, such as granting a $2.43 million cash Short-Term Incentive (STI) to the Managing Director.

- AMP Limited (49% no vote): Shareholders expressed discontent with the transparency of the short-term incentive targets and found the board’s discretionary award of substantial incentives to be unwarranted, particularly in light of the company’s share price performance.

- ALS Limited (28% no vote): Shareholders deemed the retention payments granted to two senior executives to be unjustified and excessively generous.

- Treasury Wine Estates Limited (46% no vote): Shareholders expressed displeasure with the board’s exercise of discretion, allowing the vesting of long-term incentives even when certain financial targets were not achieved.

Other examples include:

- BrainChip Holdings Limited (52% no vote): A protest vote was registered due to the company’s performance. As the chairman articulated, the company has not yet achieved any substantial progress in terms of generating revenue.

- Atlas Arteria Holdings Limited (51% no vote): A protest vote was cast in opposition to the company’s acquisition of a two-thirds stake in the Chicago Skyway motorway. Shareholders expressed dissatisfaction with the necessary equity raise for this transaction and regarded the acquisition as being made at a price higher than the prevailing market rates.

- Perenti Limited (33% no vote): Although Perenti delivered healthy returns to its shareholders, it received a strike due to apprehensions about safety precautions.

We will continue to provide updates as the majority of AGMs are held over the next month.

Once again we have undertaken research to understand what subsequent actions (if any) have been taken by ASX300 Companies which received a ‘strike’ on their Remuneration Report in 2022.

Of the 16 companies who received a strike last year, 13 (81%) made changes to address either some or all of the concerns raised by shareholders and / or proxy advisor groups. The remaining 2 companies have not indicated any changes in response to the shareholder concerns (Dicker Data Limited and Lovisa Holdings). Note it is a requirement under the Corporations Act 2001 that the company’s remuneration report include either a description of the actions the board intends to take in response to a ‘strike’ or an explanation of the reasons for taking no action.

Strike Responses Tracker

Unlike prior years, company responses to ‘strikes’ in 2022 comprised of multiple changes (up to four) to address shareholder concerns (perceived or known). As an example, to strengthen performance and reward alignment, changes were made to performance measures and weighting, introduction of minimum shareholding requirements, and the addition of gateways (e.g., EPS, TSR) in long-term incentive plans. Companies also enhanced transparency in their remuneration practices by providing additional disclosure of group-level targets, principles for applying discretion, and detailed information regarding key performance indicators (KPIs).

The chart below shows the three most common response themes adopted by companies to the ‘strike’ on their Remuneration Report.

Examples of the responses include:

- Change to variable pay structure: change in weighting (Newcrest Mining Ltd increasing the weighting of relative TSR from 33% to 50% and reducing the weighting of both ‘Return on Capital Employed’ and ‘Comparative Cost’ from 33% to 25%), increasing the LTI performance period (Corporate Travel Management Ltd from 2 years to 3 years), the replacement of Options with Restricted Stock Units or Performance Rights (Imugene Ltd).

- Change to disclosure: providing additional disclosure on group level targets (Downer EDI Ltd), adding more details regarding the STI plan (Lake Resources NL) and including more detailed information in relation to Executive KMP performance (Link Administration Holdings Ltd).

- Change to quantum: reducing the Non-Executive Director base and committee fees (The Star Entertainment Group Ltd), reducing the quantum of LTI awards by 10% (Goodman Group), setting the fixed remuneration of the new CEO lower than the predecessor’s (Downer EDI Ltd).

| *What is a strike?

If a company’s remuneration report outlining salary and incentives of key management personnel (KMP) receives a ‘no’ vote of 25% or greater from shareholders at the annual general meeting, the company receives a first ‘strike’. If the following year’s remuneration report also receives a ‘no’ vote of 25% or more, the company receives a second ‘strike’. When a second ‘strike’ occurs, shareholders vote then and there to decide whether company directors must stand for re-election. This is known as a ‘spill’ vote. If the spill vote passes (i.e., 50% or more of eligible votes cast), a spill meeting is held within 90 days and the directors stand for re-election. See our blog “10 Years On Does The 2 Strikes Law Really Matter?” for more information. |

2022

In the wake of the war in Ukraine, rising interest rates, supply chain disruptions and the decline in macroeconomic sentiment, the backdrop for this year’s 2022 AGM season was anticipated to be a challenging one for companies seeking investor support on their Board and executive remuneration practices. As 2022 AGMs wrap up, the resulting headline is somewhat different – the highest level of remuneration support for Australia’s largest 300 companies we have seen in 5 years (at least)! For the ASX300 this year, a total of 18 companies (8%) received a ‘strike’ on their remuneration report which is down from 24 companies (10%) in 2021.

What’s causing these results? It’s potentially due to a number of reasons!

- Companies are getting better at disclosure: The improved voting outcomes in 2022 could be partly due to companies becoming more effective in the way information is disclosed in the remuneration report. Each year, TRP reviews approximately 200 company remuneration reports and scores them across three categories being Readability, Accuracy and Disclosure. In 2022, the Disclosure category improved by almost 50% compared to 2021. This was driven by enhanced reporting of the “what, how and why” of remuneration and which may be implemented through the introduction of a chair letter, detailed executive KPI’s including targets and stretch targets and detailed rationale in the case of applied discretion.

- ‘One-off’ awards and uncommon pay structures less prevalent: During 2020 and 2021, we observed an increase in the usage of one-off retention awards, increased reliance on discretion regarding payout/vesting outcomes and service-only vesting conditions in response to the COVID-19 pandemic. All responses we know have attracted heightened concern from investors and increased the likelihood of a vote against the remuneration report. In 2022, remuneration changes in response to COVID19 have all but ceased with limited instances of special awards and Board discretion applied.

- 2022 was less eventful than 2021: Looking back on remuneration report voting since 2011 (when the ‘two strikes rule’ was introduced) ‘no votes’ have varied. What seems to be consistent though is higher instances of ‘no’ votes tend to follow significant legislative change (e.g., Financial services inquiry) and/or economic shocks (e.g., COVID-19) where companies are more likely to revise remuneration approaches in response therefore increasing the level of shareholder scrutiny. No doubt 2022 has provided companies with many challenges for all the reasons noted above however less so than the pandemic fall out in 2021 which arguably provided greater reason for investor anxiety.

Whilst the 2022 AGM season has resulted in higher levels of investor support on board and executive remuneration than previous years, opportunities remain for improvement (particularly for the 7% of ASX300 companies that received a ‘strike’ and the 6% who narrowly missed receiving a ‘strike’).

You can our analysis for the 2022 ASX300 remuneration report voting results.

Companies should not underestimate the impact of a substantive ‘no’ vote on the remuneration report.

We know from past research that there is a potential correlation between company performance and ‘no’ votes on the remuneration report. In fact, our research over a four year period showed there is almost a 50% chance of a company’s share price falling on average 30% following a ‘strike’ on the remuneration report (see our blog 10 Years On, Does The ‘Two-Strikes’ Law Really Matter?).

Our ongoing discussions with Boards and Remuneration Committees reflect a difficult economic outlook in 2023 and opportunities to ensure remuneration practices are well placed across the organisation. We will keep you apprised of what unfolds in coming months.

As the 2022 AGM season marches on, we continue to track shareholder voting on the Remuneration Report for ASX300 companies. To date, a total of 194 ASX300 companies have had shareholders vote on their Remuneration Report. Figure 1 below shows a year on year comparison of the percentage of ASX300 companies which have received a “strike” (greater than 25% of eligible shareholders voting against) or a “near miss” (between 15% to 25% of eligible shareholders voting against) on their Remuneration Report. The results to date indicate a continued downward trend from recent years.

Figure 1. Voting outcomes in 2022 to date compared to prior years

The main themes for “strikes” on Remuneration Reports to date largely centre around a misalignment between performance, remuneration outcomes and shareholder expectations. Some examples include:

- Downer EDI received a 56% no vote. Shareholder concerns over a number of remuneration outcomes, including the board’s decision to use its discretion to award executives’ short-term bonuses despite the company failing to meet the profit gateway.

- Blackmores received 43% a no vote. Shareholders opposed the short term and long term grants due to poor share price performance and earnings per share (EPS).

- Newcrest received a 37%% no vote. Shareholder concerns that the bonuses paid to the chief executive were overly generous compared to the company’s financial performance.

- ASX received 31% no vote. Shareholders opposed the executive incentive payout made despite the delays in the trade settlement system project.

- AGL received 31% no vote. Shareholders wanting to see a greater alignment of remuneration structure with company performance and long-term shareholder value.

Other themes for “strikes” include:

- Generous retention incentives: For example, Santos received a 25.3% no vote as one of the proxy advisors view the $6m one-off retention incentive awarded to CEO “excessive”. Corporate Travel Management received a 33% no vote as the shareholders opposed the long term incentive (LTI) put in place to retain key executives during COVID.

- Appropriateness of performance hurdles and assessment: For example, Goodman Group received a 28.9% no vote due to the EPS hurdles being considered not sufficiently challenging from the perspective of proxy advisors. In particular,, there was criticism regarding the adoption by the board of an “economic value approach” to assessing the earnings hurdle rather than the “face value approach more commonly used by the market”.

We anticipate wrapping up our final observations on the 2022 AGM season for ASX300 companies before the Christmas break.

Our observations of responses to ‘strikes’ indicate that most companies (20/24) have made changes to adress either some or all of the concerns raised by shareholders and / or proxy advisor groups. These changes ranged from structural redesign of the incentive plan to enhancing the disclosure and transparency (particularly in terms of performance measures and outcomes). Some specific actions companies have taken include:

- Increased stretch regarding incentive plan performance conditions and targets (IDP Education, Dexus, Link Administration, Goodman, Appen)

- Enhanced disclosure, particularly in terms of performance outcomes ( Megaport, Insurance Australia Group, Platinum Investment Management.)

- Introduction of a minimum shareholding requirement for executives and NEDs, with between 50% – 300% of fixed remuneration for NED’s & Other KMP (Whitehaven, Dicker)

- Changes to variable pay plan structures such as the introduction of an STI & LTI cap (Platinum Investment Management.), the introduction of a Single Incentive Plan to replace the STI & LTI (Whitehaven) and the replacement of Options with restricted stock units (RSUs) by Megaport

Strike Responses Tracker

A total of 24 ASX300 companies recorded a ‘strike’ against their Remuneration Report in 2021. We have grouped responses to the ‘strike’ into 7 main categories which are illustrated in the chart below.

Main response categories

- No changes in response to shareholder concerns

- Change to variable pay structure (E.g.,changes to award vehicle, vesting period or vesting schedule)

- Change to performance conditions (E.g, changes to measures, weightings)

- Change to quantum (E.g., reduced fixed remuneration or STI/LTI opportunity or max. opportunity, NED fees)

- Formalising use of discretion (E.g., framework or formal approach disclosed)

- Disclosure/communication enhanced (E.g., improvement in disclosure of STI outcomes from prior year)

- Other (E.g., introduction of minimum shareholding requirement)

| *What is a strike?

If a company’s remuneration report outlining salary and incentives of key management personnel (KMP) receives a ‘no’ vote of 25% or greater from shareholders at the annual general meeting, the company receives a first ‘strike’. If the following year’s remuneration report also receives a ‘no’ vote of 25% or more, the company receives a second ‘strike’. When a second ‘strike’ occurs, shareholders vote then and there to decide whether company directors must stand for re-election. This is known as a ‘spill’ vote. If the spill vote passes (i.e., 50% or more of eligible votes cast), a spill meeting is held within 90 days and the directors stand for re-election. See our blog “10 Years On Does The 2 Strikes Law Really Matter?” for more information. |

2021

With AGMs now wrapped up for the calendar year 2021 we look back on executive remuneration, the key takeaways and perhaps some clues for what’s ahead in 2022.

Key Takeaways

- Shareholder ‘no’ votes on Remuneration Reports close to long term trend – a total of 10% of ASX300 companies recorded a ‘strike’ on their Remuneration Report in 2021 (see Fig 1 below). This outcome is relatively consistent with the long term trend of 9% of companies per year since the ‘two strikes rule’ was introduced back in 2010. Reasons for shareholder concerns this year range from performance measures not challenging enough (e.g., Whitehaven Coal), poor disclosure (e.g., Scentre) and of course protest votes relating to broader company issues (e.g., Westpac)

- Total remuneration above pre-covid levels with boost from incentives – whilst fixed remuneration generally regained what was lost over the last couple of years, short term incentive (STI) payouts were plentiful and long term incentives (LTI’s) values benefited from rebounding share prices. Our analysis of a sample of 150 ASX company CEO’s (all sectors all sizes) noted a median increase in total remuneration of 28% (fixed + STI + LTI).

- Exercising discretion having mixed results – shareholders seemingly welcoming ‘negative’ discretion reducing payouts for executives (FMG removed STIs for management following Ironbridge project issues; Ansell (adjusting STI payouts downwards following windfall gains). Those companies that exercised ‘positive’ discretion resulting in favourable outcomes for executives included Dexus (expected adjustment to recognise impact of increased funds from operations).

- ESG featuring in incentives – now moving beyond just a ‘fad’, environmental social governance (ESG) is now featuring in more executive remuneration programs. This year we have seen a number of companies across industry sectors feature ESG metrics in short and long term incentives including South32 (safety, community and climate change), Champion Iron (GHG emissions), Endeavour (responsible sale of alcohol), Goodman Group (environmental and sustainability hurdles).

- Executive retention awards on the radar – a topic of great interest this year as companies looked to shore up their key talent. Our analysis of a sample of 150 ASX companies (all sectors all sizes) noted approximately one quarter made a retention award this year with most in equity which vested over 2-3 years. Examples included Stockland, Webcentral, Energy Resources of Australia and Ampol.

As companies now shoulder into a more positive short-term outlook with boarders re-opening (albeit with some navigation required through supply chain disruptions) what seems apparent for executive remuneration is likely heightened scrutiny where payments are not aligned with shareholder and community expectations.

As the AGM season marches on, we continue to track shareholder voting on the Remuneration Report for ASX300 companies. To date there has been 169 ASX300 companies who have had shareholders vote on their Remuneration Report.

The percentage of companies (from the ASX 300) which have received “strikes” (greater than 25% of eligible shareholders vote against) or “near misses” (between 15% to 25% of eligible shareholders vote against) on their Remuneration Report voting is trending slightly lower than 2020. Figure 1 illustrates voting outcomes in 2021 to date compared to prior years.

Fig 1.

So what are the themes surrounding the voting?

- Performance and pay misalignment – the payment of incentives despite the company making a loss or not performing as well as expected

-

-

- Whitehaven: Executives awarded STI payments despite company receiving three production downgrades.

- Transurban: Bonuses and sign-on grants were seen as excessive given the decline in income over the 12 month period.

- Insurance Australia Group Limited: Paying of bonuses despite management errors that cost the company more than $1.5 billion.

-

- Protest votes – more about company performance than just remuneration

-

-

- Crown Resorts: Lingering governance issues.

- Rio Tinto: Investor concerns over last year’s destruction of ancient rock shelters in Western Australia.

-

Some other unique company circumstances:

- Technology One: Disapproval of Board discretion of LTI vesting despite targets not being achieved.

- Transurban: ‘Executive-specific’ measures for STI’s deemed inappropriate and as part of their job.

With 30 June year end annual reports now released, our latest analysis of the ASX300 provides insights on the various measures taken (or not) by those companies who received a ‘strike’ on their previous remuneration report. Though the response details did vary based on company’s individual context, some interesting themes emerged.

Most companies responded with several changes

While ‘changes to variable pay structure’ and ‘enhancing disclosure’ were the responses most used, the majority of companies (approx. 75%) used a combination of responses. Almost 60% of companies implementing a change in pay structure also had a change in quantum as part of their response. We noted only two companies responded with a change in pay structure only.

Some companies didn’t respond at all

Although an acknowledgement of (and response to) the strike is a requirement under the Corporations Act, three companies failed to disclose changes in response to their strike. Whilst a legislative requirement should provide reason enough for companies to take action, the broader implications of a ‘strike’ on the remuneration report for boards and executives can be profound including reputational damage and the potential of loss in enterprise value.

Plenty of changes in variable pay structures

With pay and performance misalignment being shareholders’ top concern from our research last year approximately six in ten companies responded to their strike by changing elements within their variable pay structure. For example, AMP increased the deferral component of their STI from 40% to 60% while Carnarvon Petroleum, Lendlease Group and Sigma Health also introduced deferral components ranging from 25% – 50%. STI performance measures were also tweaked in response to shareholder concerns with Bapcor increasing the emphasis on ESG metrics and AP Eagers and Accent both restructuring their incentive plans with a balance of financial and non-financial metrics.

Increasing transparency and enhancing disclosure

Enhancing communication of remuneration details is also a key concern of shareholders and was the second most popular response, with a third of the companies pledging to provide a more detailed disclosure. There are various aspects to remuneration transparency and disclosure may have different points of focus for individual organisations. For example Inghams Group aims to improve its transparency through disclosure of LTI targets retrospectively; Clinuvel Pharmaceuticals has decided to provide transparency to measures not market sensitive whilst Ive Group and Mount Gibson Iron have also disclosed more detail relating to their incentive payments.

Though increasing disclosure of remuneration components is a popular reaction among those who have received a strike, interestingly TRP analysis of ASX300 Remuneration Reports shows the level of disclosure has not changed substantially in relation to previous years. The level of disclosure in FY21 is almost at an identical level to what it was in FY20, perhaps indicating some boards’ reluctancy to change unless ‘poked’ by some aggrieved shareholders.

Metals & Mining CEO Remuneration Updates

As company reports continue to roll in, we ran some early analysis to understand remuneration changes for CEOs of Metals & Mining Sector companies who have been in the same role for the last two years.

What is the data is telling us?

- Fixed pay increases on average 7% – with the backdrop of some catch up footy from little to no pay increase in 2020, and most commodities having a sterling run over the last year (which has been largely translated into significant TSR movements), many CEOs in our sample have seen substantive increases. Estimates from our May 2021 Pulse Survey indicated 2-3% which is well below the actual data from the sample to date

- Reduced number of maximum Short term incentive payouts – 17% of companies from the sample awarded the CEO 100% of maximum STI, well short of the 28% we saw from the same group of companies last year. Given the strong performance of the sector, this was a surprising outcome and may reflect boards exercising downward discretion in consideration of factors beyond the scheme mechanics

- Increased LTI grant value – the overall levels of LTIs awarded were higher than the previous year. When looking at the value of LTI grants as a percentage of base salary, there is a noticeable increase in the average, from 82% in 2020 to 98% in 2021.

More detailed breakdown of the TRP database will be provided later in the year and upon the completion of the reporting season. This will include analysis of TRP 150 (comprising all sectors) and the ASX300 Metals and Mining Index.

YTD Remuneration Report Voting Outcomes

As at 10 September 2021

Below we’ve charted the Remuneration Report voting outcomes of 43 ASX300 companies for the 2021 AGM season to date. So far we have noted slightly higher instances of strikes and near misses than in previous years. We will provide another update as results come to hand.

Our observations of responses to ‘strikes’ indicate most companies (20 out of 23) have made changes ranging from significant structural redesign to enhancing the disclosure and transparency (particularly with hurdles relating to incentive plans). Some specific actions companies have taken include:

- Enhanced disclosure – in addition to greater supporting rationale for ‘why’ remuneration approaches have been adopted. ING, for example has included disclosing targets for past STI awards.

- Governance – a growing trend to introduce a minimum shareholding requirement for executives and NEDs typically around 100% of fixed remuneration (Bapcor, ING, Sigma)

- LTI – increasing performance periods from 3 years to 4 years (AP Eagers, Northern Star, Sandfire).

- STI – introducing deferral (LendLease, Sigma Health) and gateways (Carnarvon Petroleum – share price, QUBE – safety)

Strike Responses Tracker

A total of 28 ASX300 companies recorded a ‘strike’ against their Remuneration Report in 2020. We have grouped responses to the ‘strike’ into 6 main categories which are illustrated in the chart below.

Main response categories

- No changes in response to shareholder concerns

- Change to variable pay structure (E.g.,changes to measures, weighting, performance period or vesting schedule)

- Change to quantum (E.g., reduced fixed remuneration or STI/LTI opportunity or max. opportunity, NED fees)

- Formalising use of discretion (E.g., framework or formal approach disclosed)

- Disclosure/communication enhanced (E.g., improvement in disclosure of STI outcomes from prior year)

- Other

| *What is a strike?

If a company’s remuneration report outlining salary and incentives of key management personnel (KMP) receives a ‘no’ vote of 25% or greater from shareholders at the annual general meeting, the company receives a first ‘strike’. If the following year’s remuneration report also receives a ‘no’ vote of 25% or more, the company receives a second ‘strike’. When a second ‘strike’ occurs, shareholders vote then and there to decide whether company directors must stand for re-election. This is known as a ‘spill’ vote. If the spill vote passes (i.e., 50% or more of eligible votes cast), a spill meeting is held within 90 days and the directors stand for re-election. See our blog “10 Years On Does The 2 Strikes Law Really Matter?” for more information. |

About This Resource

Leveraging data and tools from our research platform, The Reward Practice has developed this yearly resource for the ASX reporting season to keep you updated on key ASX300 executive remuneration and governance insights as they happen.

Data is gathered from Remuneration Reports, and translated into our weekly commentary including insights relating to:

- Remuneration structures – how prevalent will companies use retention grants to manage an uncertain future? Is deferring some/all of STI growing in prevalence as companies seek to manage unforeseen events?

- Fixed remuneration – with many companies restraining pay last year, some industries now experiencing growth and retention concerns, will we see material fixed pay increases?

- Incentive measures – will non-financial measures adopt greater weighting in STI and LTI plans? Environmental, Social, Governance (ESG) is a key consideration but how will it feature within executive incentive plans?

We have also developed an ASX300 Remuneration Report tracking tool to provide insights on:

- Rem ‘strike’ responses – company responses on remuneration matters since receiving a ‘strike’ last year

- Shareholder voting outcomes – how shareholders have responded to 2024 Remuneration Reports including ‘strikes’ and near misses

- Remuneration Report quality – who is doing it better than others? Our assessment of the 2024 Remuneration Report readability, accuracy and disclosure

The aim is to monitor and consolidate remuneration concerns, trends and actions and have this page serve as an informational reference for our readers as the reporting season progresses.