The lead up to the annual reporting season presents a valuable opportunity for companies to review their executive remuneration programs and disclosures. Reviewing these policies may help avoid a strike (and possible board spill), but is also essential to ensure they are relevant, competitive and add value to the organisation. Directors owe broad fiduciary responsibilities to companies they serve, particularly under the Corporations Act 2001 and the common law. This duty extends to the remuneration of Key Management Personnel, ensuring it is in the best interests of the company.

‘Two strikes” Rule

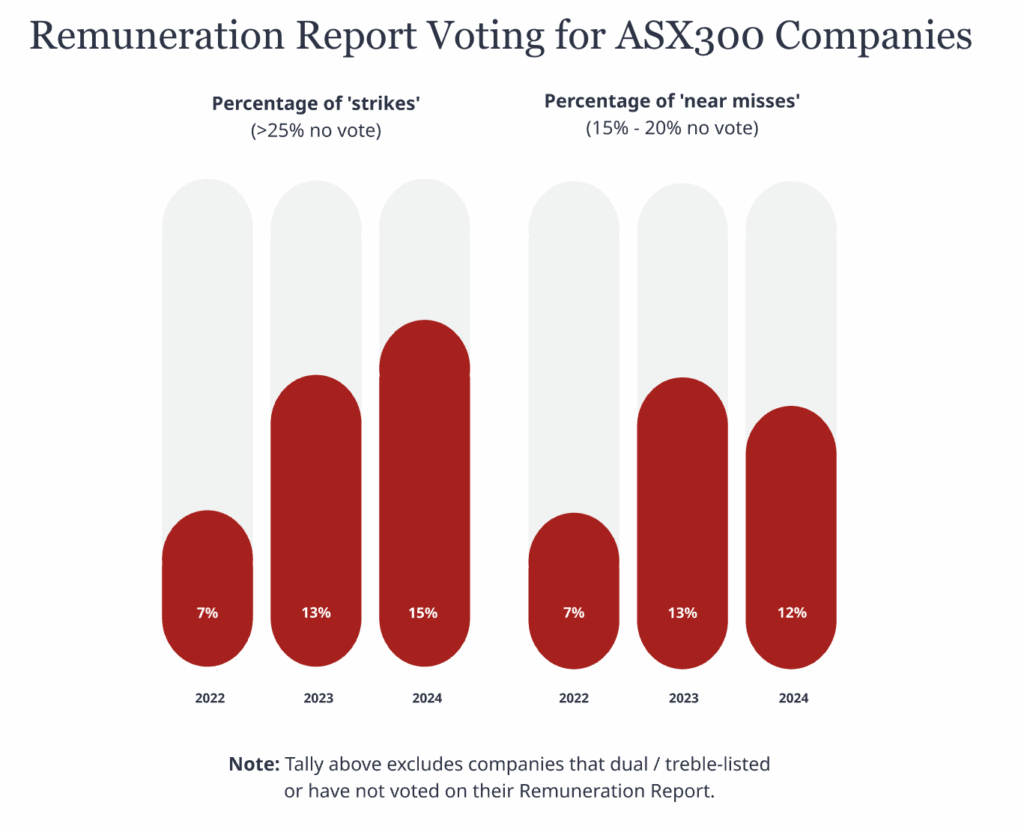

In 2011, amendments to the Corporations Act introduced the “two strikes” rule. This regulatory change brought the spotlight back onto directors, holding them accountable for the salaries and bonuses of executives.

- Two consecutive “strikes” can lead to a board spill, which can then create organisational instability.

- ASX300 – 18 strikes and 40 significant “no” votes. Significant “no” votes have increased 38% since the previous year.

Most prevalent reasons for poor outcomes:

Voting seasons provide themes in relation to the reason for “strikes” being received. Many of these appear to be regular issues in recent years.

- Pay and performance – misaligned to market levels

- Communication is unclear – Inadequate disclosures to shareholders

- Disagree with business which has nothing to do with remuneration – Considered a protest vote

Although you cannot control number three, the first two reasons can be addressed in the lead up to the remuneration report being released. Flag any unusual or contentious pay and performance metrics in your remuneration report, with guidance on intended future changes. Communication should be an ongoing and consultative process, particularly involving proxy advisors and key shareholders. Drafting a more effective remuneration report with peer insights will also help communicate the reasoning behind your executive pay policy.

Prevention / Actions to take

- Go beyond the minimum requirements of statutory disclosure will help shareholders understand the reasoning behind the Key Management Personnel (KMP) remuneration, enabling them to make a more informed decision about the remuneration report. This can lead to better outcomes for organisations, potentially avoiding shareholder backlash and negative publicity which can result from a “strike” against a remuneration report.

- Include an Executive Summary

Although not explicitly required in the disclosure rules, there has been positive feedback for companies introducing their remuneration report with an Executive Summary (or “Letter from the Remuneration Committee Chair” to shareholders) setting out: company key performance outcomes and resultant KMP remuneration for the year, listing significant changes to the structures during the year such as KMP, STI or LT structure changes. This disclosure is often raised at AGM’s as a positive message – due to the growing complexity of remuneration reports, providing the key messages in a few easy to read paragraphs. - Describe benchmarking methodology

When using a peer group or industry survey to benchmark KMP remuneration levels, as a minimum under section 300A of the Corporations Act, disclose objective and/or subjective selection criteria used to establish the peer group to support the appropriateness of each constituent company. This may include parameters such as company size, geographical footprint and industry group. For companies that position KMP remuneration levels at a certain percentile of the competitive market, such as market median or above-market remuneration, the disclosure should fully and transparently articulate the rationale as to why such a philosophy is appropriate. - Outline performance measures and goals

In accordance with section 300A(1)(ba) of the Corporations Act, if an element of the remuneration is dependent on the satisfaction of a performance condition, there are a number of detailed disclosures the company should provide. Particularly, summarising the performance condition, reason for its use and an overview of the method used to assess whether the performance condition was satisfied. It is also good practice to allow shareholders to understand the threshold, target and maximum levels for performance goals.

- Include an Executive Summary

- Taking a proactive approach to engaging with large shareholders and proxy advisors throughout the year will prove to be a more effective way of canvassing the opinions of these groups, explaining the company’s position on these issues and maintaining their support once changes have been implemented.

- Plan using a calendar to agree and track activities including; a shareholder engagement approach; formulating an “issues and considerations” register of stakeholder views, responses and risks; development of a remuneration report structure including layout and style; drafting the remuneration report with necessary governance procedures including audit and board sign off.